Should You Build a One-Month Emergency Fund Before Paying Off Credit Card Debt?

Should you build a one-month emergency fund before paying off credit card debt? Here is the real tradeoff, with numbers, payoff math, and when the bigger buffer makes sense.

Should You Build a One-Month Emergency Fund Before Paying Off Credit Card Debt?

If you are trying to decide whether to build a one-month emergency fund before paying off credit card debt, the honest answer is: usually yes—if your current cash buffer is too small to handle normal life without new borrowing.

A lot of debt payoff advice jumps straight from “save $1,000” to “throw every extra dollar at debt.” That can work for some households. But if your rent, groceries, utilities, and transportation take most of your paycheck, a one-month emergency fund can make the debt plan a lot more durable.

This is not about hoarding cash while high-interest debt grows. It is about building enough breathing room that one bad month does not send you right back to the credit card.

The core tradeoff

When you keep more cash in savings, you usually:

- pay debt off a little slower

- pay somewhat more total interest

- reduce the odds of needing to borrow again during a setback

When you keep almost no cash and go hard on debt, you usually:

- pay debt off faster on paper

- save interest if nothing goes wrong

- take more risk that the next emergency or income dip restarts the cycle

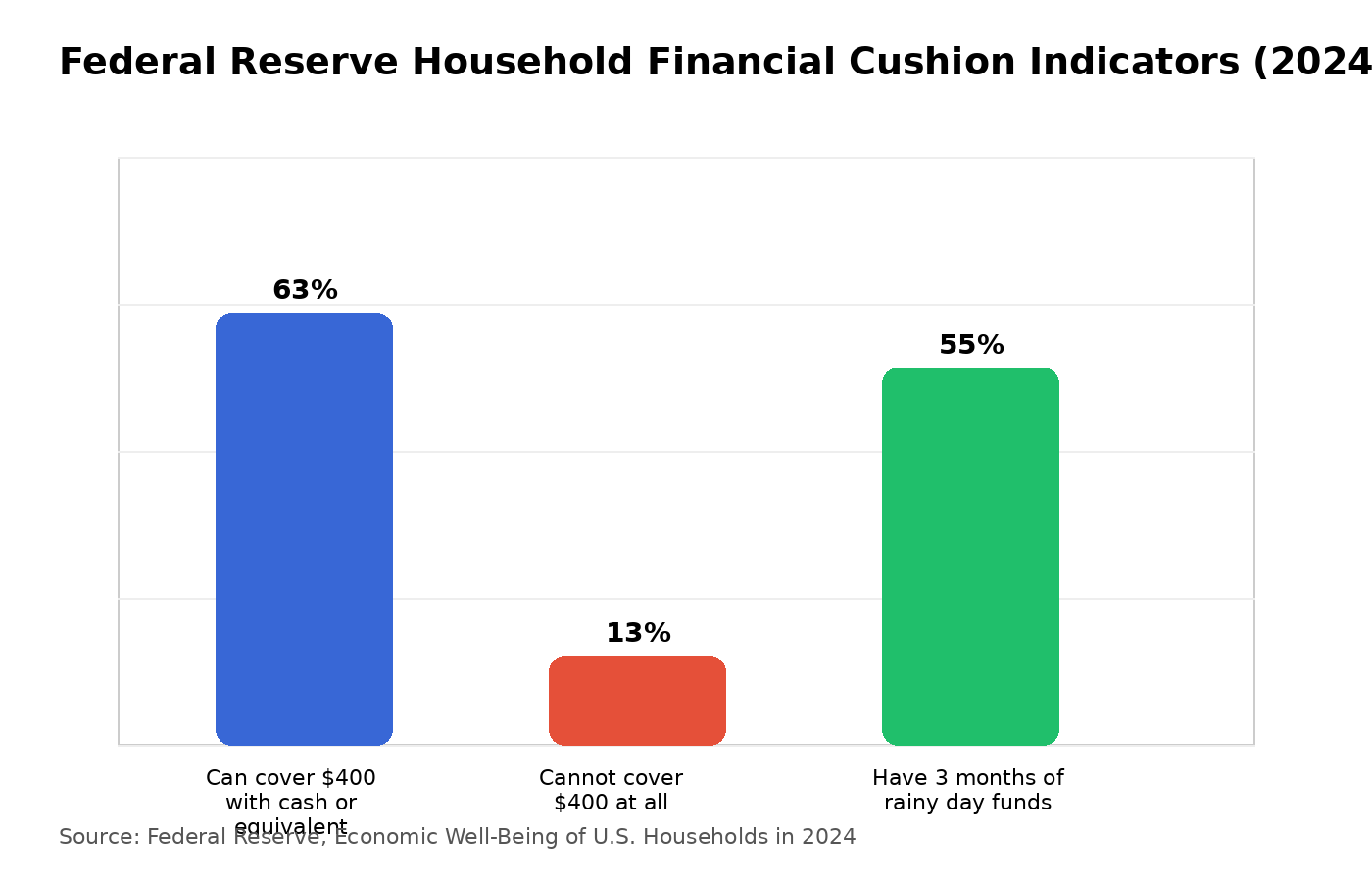

That tradeoff matters because financial shocks are common. In the Federal Reserve's 2024 household well-being report, 63% of adults said they would cover a $400 emergency expense with cash or the equivalent, while 13% said they would not be able to cover it at all. The same report said 55% had rainy day funds to cover three months of expenses. Those numbers are a reminder that cash buffers still matter, even when debt is expensive.

The CFPB makes the same practical point: even a small emergency fund can help you recover faster from an unexpected expense and avoid taking on more debt.

So should you build a full month of expenses first?

Not always.

But I think a one-month emergency fund is often the right intermediate target when one or more of these are true:

- your income is irregular or seasonal

- you have kids or a household with higher surprise costs

- your car is older and you rely on it for work

- your current starter fund is tiny compared with your monthly bills

- you keep running into “temporary” setbacks that go back on the card

If your job is very stable, your bills are low, and you already have a reliable support cushion, then a smaller starter fund may be enough while you attack debt faster.

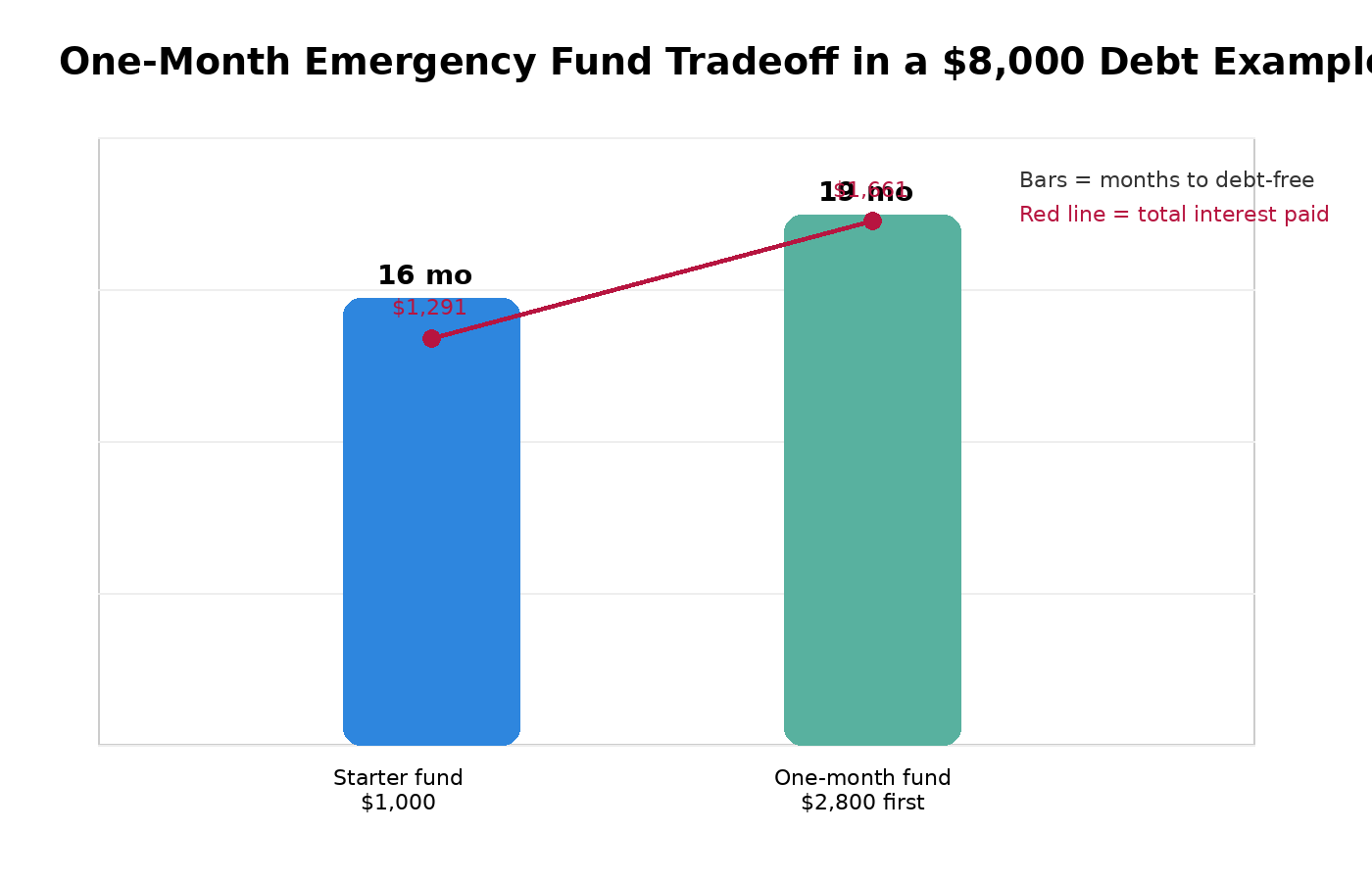

A realistic example with numbers

Let’s say your monthly essentials are:

- Rent and utilities: $1,450

- Groceries: $550

- Transportation: $300

- Insurance and phone: $250

- Minimum debt payments: $250

That puts your essential monthly outflow at $2,800.

Now assume you have:

- $8,000 in credit card debt at 24% APR

- $1,000 already saved

- $600 per month available to direct toward either savings or debt above your other essential bills

You are choosing between two strategies.

Strategy A: Stop at $1,000 and attack debt now

- Keep starter emergency fund: $1,000

- Put the full $600/month toward the card immediately

Strategy B: Build one month of expenses first

- Savings target: $2,800

- Additional savings needed: $1,800

- Put $600/month into savings for 3 months first

- Then redirect the same $600/month to debt payoff

Strategy B clearly delays the debt attack. But it also means that if your transmission, deductible, or income dip hits during the first few months, you have a much better chance of absorbing it without adding fresh debt.

What the math looks like

Using standard monthly compounding at 24% APR:

- Strategy A pays the card off in about 16 months and costs about $1,291 in interest.

- Strategy B takes about 19 months total from today because the first 3 months go to building the one-month fund, and total interest is about $1,661.

- The cost of building the one-month buffer first in this example is roughly 3 extra months and about $370 more interest.

That is real money. So why would anyone choose Strategy B?

Because the spreadsheet only wins if life cooperates.

If a $1,500 car repair or short paycheck lands while you only have $1,000 saved, Strategy A can fall apart. If that same event hits while you have a full month of essentials in cash, you may stay on plan.

Why the “slower” plan can still be smarter

Debt payoff is not only about minimizing interest. It is about finishing.

A plan that looks optimal but keeps breaking is not actually optimal.

A one-month emergency fund can help you:

- avoid swiping the card for normal emergencies

- keep minimum payments current during a bad month

- reduce panic-driven money decisions

- stay consistent enough to keep the debt balance moving down

This matters even more if your life has a lot of moving parts. A single adult with a stable salary and paid-off car can tolerate more risk than a family of five with variable income and two older vehicles.

When a one-month fund probably makes sense

A one-month emergency fund before aggressive debt payoff is often reasonable if:

1. Your monthly essentials are much higher than your starter fund

If your essential bills are $3,000 and your cash buffer is only $1,000, that is not really a full shock absorber. It is a speed bump.

2. You have irregular income

Freelancers, commission-based workers, self-employed households, and seasonal workers often need more than a tiny starter fund just to keep month-to-month cash flow steady.

3. Your past pattern is “pay debt, then use debt again”

That is one of the clearest signs that your buffer is too small for your real life.

4. You are supporting kids or other dependents

Bigger households usually have more surprise costs. Math is not the only factor, but it is still a factor.

When you should probably attack debt sooner instead

A one-month emergency fund may be more than you need before debt payoff if:

- your job is stable and predictable

- you already have access to a small but reliable cushion

- your monthly essentials are relatively low

- you are extremely motivated and want the fastest payoff path

- the debt APR is very high and new borrowing risk is genuinely low

In that case, you may be better off keeping a smaller starter fund and going hard at the highest-interest balance.

A simple framework to decide

Here is the framework I would use:

Keep a smaller starter fund if all three are true

- your income is stable

- your monthly essentials are low relative to your savings

- you are not repeatedly falling back into debt after setbacks

Build toward one month of essentials first if any of these are true

- your income fluctuates

- your current buffer would not cover a normal bad month

- your household has frequent surprise expenses

- you have already proven that a tiny emergency fund is not enough

Best way to do it without stalling forever

If you decide to build a one-month emergency fund first, do not drift.

Use a short, explicit sprint:

- calculate one month of essential expenses

- subtract what you already have saved

- set a deadline or monthly target

- pause aggressive extra debt payments only until that target is reached

- once the fund is built, redirect the same money to debt immediately

In the example above, that means three focused months to build the fund, then an automatic switch to payoff mode.

That is very different from keeping cash in savings indefinitely while making tiny debt progress.

Where Debt Freedom Planner helps

This is exactly the kind of decision that feels fuzzy until you run your own numbers.

Debt Freedom Planner can help you compare:

- a $1,000 starter fund

- a one-month emergency fund

- different extra payment amounts

- different APR and minimum payment combinations

When you can see your debt-free date, interest cost, and payment path side by side, it gets a lot easier to decide whether the extra buffer is worth the delay.

If you want the cleanest answer, plug your real numbers into Debt Freedom Planner and compare both versions of the plan.

Bottom line

Should you build a one-month emergency fund before paying off credit card debt?

For a lot of households, yes—especially if your current starter fund is too small for the kind of setbacks you actually face.

You will probably pay somewhat more interest and take a little longer. But if that extra buffer keeps you from going back into debt, it can still be the wiser move.

The best debt payoff plan is not just the one that wins in a perfect month. It is the one that still works in a messy one.

Sources

- Federal Reserve Board, Report on the Economic Well-Being of U.S. Households in 2024 – Savings and Investments: https://www.federalreserve.gov/publications/2025-economic-well-being-of-us-households-in-2024-savings-and-investments.htm

- Consumer Financial Protection Bureau, An essential guide to building an emergency fund: https://www.consumerfinance.gov/an-essential-guide-to-building-an-emergency-fund/

0 comments

Ask a question, add context, or share what worked for your household.

Create a free account or sign in to comment, reply, and vote on blog posts.